Adeia (ADEA)·Q4 2025 Earnings Summary

Adeia Delivers Record Q4 as Disney Deal Drives 8% Revenue Beat

February 23, 2026 · by Fintool AI Agent

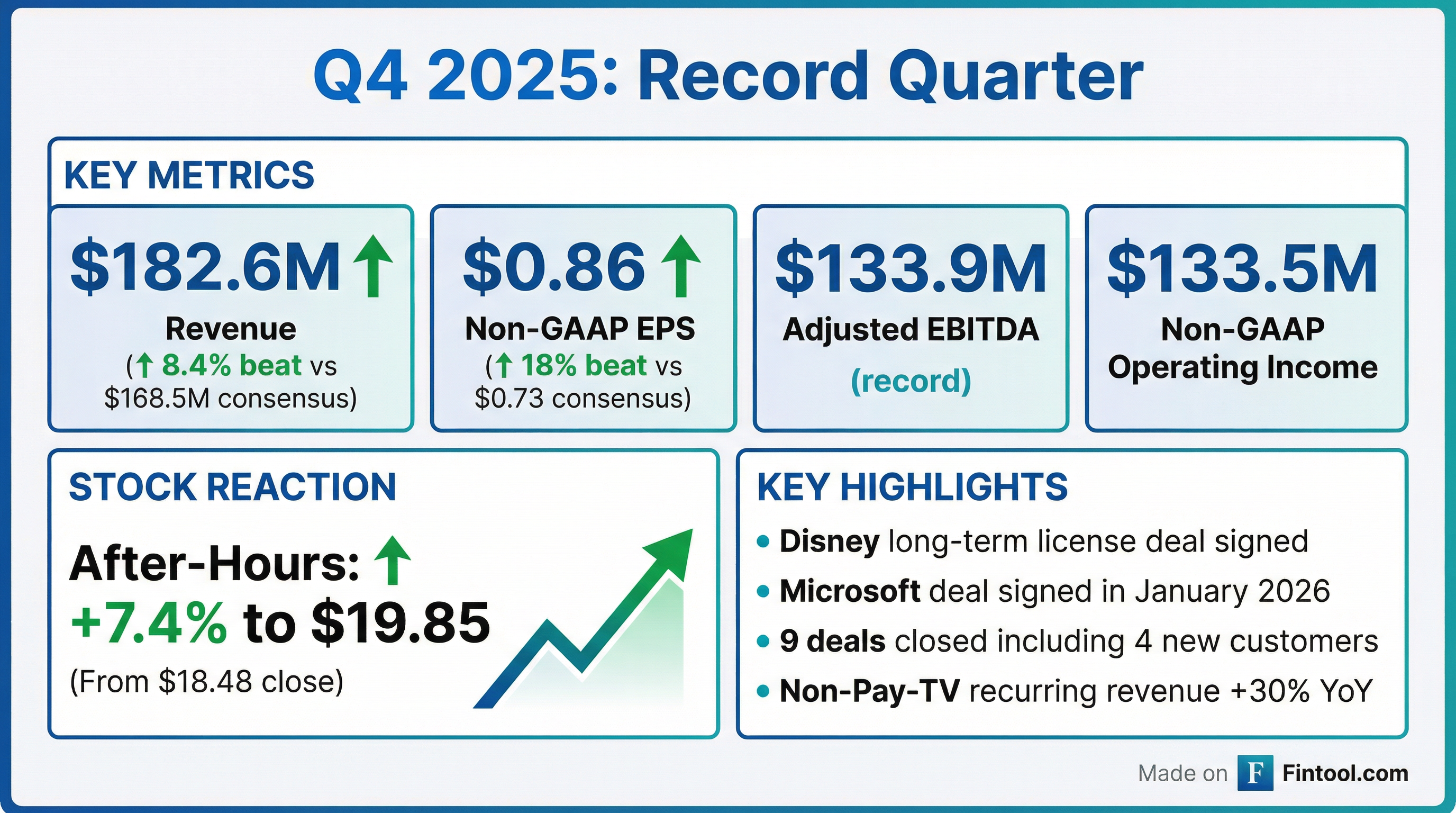

Adeia (NASDAQ: ADEA) reported record Q4 2025 results that handily beat Street estimates, driven by a landmark Disney licensing agreement. Revenue of $182.6M crushed the $168.5M consensus by 8.4%, while non-GAAP EPS of $0.86 topped the $0.73 estimate by 18%. The stock jumped 7.4% in after-hours trading to $19.85 on the news.

Did Adeia Beat Earnings?

Adeia delivered a convincing beat across all major metrics, posting record revenue, operating income, and adjusted EBITDA for the quarter:

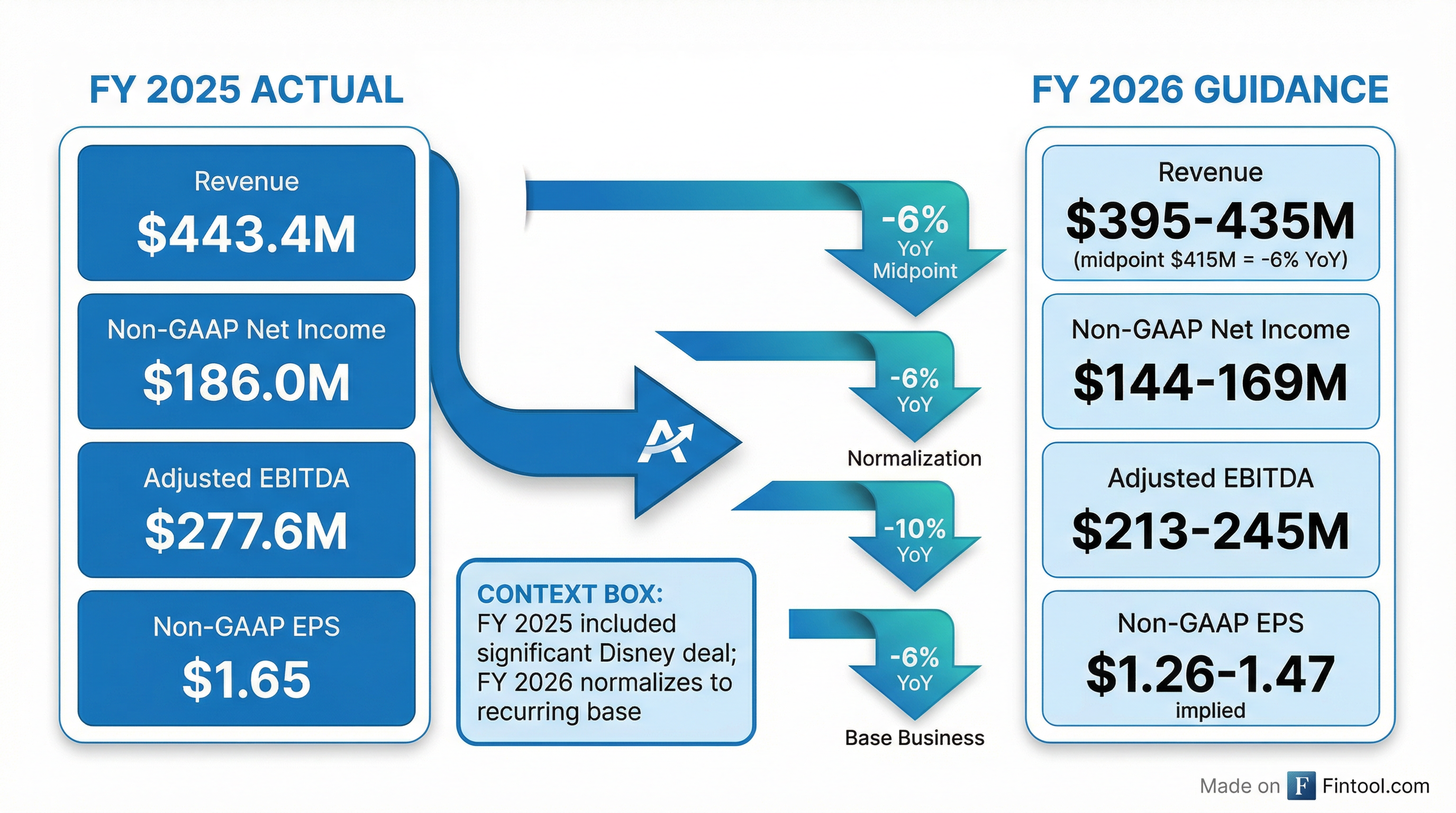

For the full year, Adeia reported revenue of $443.4M (up 18% YoY), exceeding the high end of their guidance range. Non-GAAP EPS of $1.65 for FY 2025 represented strong growth from FY 2024's $1.26.

Beat/Miss History

Adeia has now beaten EPS estimates in 4 of the last 5 quarters:

What Drove the Beat?

The quarter was highlighted by several transformative deals:

Disney Long-Term Agreement — Adeia signed a significant long-term license agreement with Disney, a leading OTT provider, resolving all outstanding litigation. This makes Disney one of the largest OTT providers now under license, joining existing customers.

Microsoft Deal (January 2026) — Post-quarter, Adeia signed a new multi-year license agreement with Microsoft for access to their media portfolio, demonstrating continued momentum into the new year.

Strong Deal Activity — The company signed 9 deals in Q4 including:

- Long-term agreement with Major League Baseball

- Multi-year renewal with Vodafone (international Pay-TV)

- New OTT customer in South Korea

- New consumer electronics customer in Japan

- Semiconductor prototype development agreement

Non-Pay-TV Growth — Non-Pay-TV recurring revenue grew 30% YoY in Q4, validating the company's diversification strategy beyond traditional cable operators.

How Did the Stock React?

ADEA shares jumped 7.4% in after-hours trading following the results:

The stock is now trading near its 52-week high, having rallied ~75% from its lows. The after-hours move suggests investors are looking past the optically lower FY 2026 guidance and focusing on the quality of deals secured.

What's Driving Revenue Mix?

The Q4 results highlighted Adeia's diversification progress and shifting revenue composition:

Key Mix Metrics from Q4:

- Q4 was nearly 50/50 recurring vs. non-recurring revenue due to Disney catch-up

- Full year 2025 was 80% recurring / 20% non-recurring

- Semiconductor revenue grew 40% YoY ($18M in FY 2024 → $26M in FY 2025)

- Non-Pay-TV recurring revenue has grown 60%+ since 2022

- OTT market share now approximately 50%

What Did Management Guide?

Adeia provided FY 2026 guidance that appears lower than FY 2025 results, but context matters:

Why the step-down? FY 2025 included significant catch-up payments from the Disney deal, which boosted Q4 2025 to $182.6M vs. the more typical $85-90M quarterly run rate. FY 2026 guidance reflects a more normalized recurring revenue base.

The company expects operating expenses of $184-192M (non-GAAP), interest expense of $34-36M, and a 21% non-GAAP tax rate.

What Changed From Last Quarter?

Several positive developments since Q3 2025:

The dramatic Q4 improvement reflects the timing of the Disney deal closing. Management also highlighted:

- Patent Portfolio Expansion: IP portfolio grew 13% YoY through internal R&D and 6 tuck-in acquisitions

- Leadership Realignment: Senior leadership team restructured for long-term scale and growth

- RapidCool Momentum: Thermal solution now being evaluated by multiple AI semiconductor supply chain participants

Capital Allocation Highlights

Adeia continued its balanced capital return strategy in Q4:

The term loan balance stands at $426.7M as of December 31, 2025, down from $487M at the start of the year. The company declared a $0.05/share dividend payable March 30, 2026.

Remaining stock repurchase authorization: $160.0M

Key Quotes from Management

Paul E. Davis, CEO:

"We finished the year with strong momentum, delivering record fourth-quarter revenue of $182.6 million, along with quarterly records in operating income and adjusted EBITDA... Notably, we entered into a significant long-term license agreement with Disney, resolving all outstanding litigation and underscoring the strength and broad applicability of our media portfolio."

"The past year was exceptional, both financially and operationally. We are very pleased that our record annual revenue, and excellent operating income and adjusted EBITDA, all exceeded the high end of our guidance range."

Q&A Highlights

On Pay TV Subscriber Trends:

"You're spot on in terms of what we're seeing with the likes of Charter and seeing an actual increase in their video subscribers. We do see some moderation in the declines as a total %, and we expect that to continue." — Paul Davis

On RapidCool Differentiation:

"What's great about our solution and what we think differentiates it is it's plug and play. You can use the same equipment that is being used today. You can put it into a liquid cooling rack and data center that is already set up for liquid cooling today." — Paul Davis

On Q4 Outperformance Drivers: CFO Keith Jones explained the beat came from three factors: (1) Disney accounting came in more favorable than initially estimated, (2) the sales team closed additional deals after Disney including MLB, and (3) favorable royalty reports from increased volume on both Pay TV and semiconductor sides.

On Microsoft Deal Materiality:

"It's a great deal for us... It's structured like many of our other non-Pay TV deals. It will be a significant customer for us." — Paul Davis

On NAND Royalty Timing: Management noted they're working through minimums from the Kioxia/SanDisk deal signed in March 2023. Revenue impact will be more pronounced in 2027 once minimums are exhausted. The company benefits from volume increases, not price increases.

On EBITDA Margin Guidance (55% vs. ~63% in FY 2025): The margin compression is driven almost entirely by higher litigation expense, expected to increase $5-10M above the $25M spent in FY 2025. R&D and SG&A remain at single-digit growth. Management views $25-35M as normalized litigation spend.

On Long-Term Target: Management reiterated their long-term goal of $500M in annual licensing revenue, with multiple paths to achieve FY 2026 guidance including both media and semiconductor opportunities.

Forward Catalysts

Looking ahead, several catalysts could drive the stock:

-

Microsoft Deal Ramp — New multi-year agreement signed in January 2026 should contribute to recurring revenue. Management expects H1 and H2 2026 to be relatively equal in revenue contribution.

-

OTT Expansion — Disney and Amazon (the two largest OTT providers) now under license. Pipeline expanding with ~50% OTT market share captured.

-

Hybrid Bonding Adoption — AMD already in production; Intel, Broadcom, and Marvell have publicly disclosed hybrid bonding roadmaps. Memory leaders (Micron, Samsung, SK Hynix) making multi-billion dollar advanced packaging investments.

-

HBM Relicensing — Memory licensing renewal opportunities coming in 2027-2028 timeframe as HBM demand accelerates faster than expected.

-

NAND Upside — As NAND approaches 400 layers, Kioxia competitors (Samsung, Micron, SK Hynix) expected to adopt hybrid bonding. Revenue from Kioxia/SanDisk deal becomes more pronounced after 2027.

-

RapidCool Opportunity — Differentiated thermal solution applicable to both logic and memory (including HBM). Plug-and-play compatibility with existing data center infrastructure.

-

Path to $500M Revenue — Long-term target with multiple paths including media momentum and large semiconductor opportunities in pipeline.

Summary

Adeia delivered a standout Q4 2025 with record revenue, operating income, and EBITDA, driven by a transformative Disney licensing deal. The 8.4% revenue beat and 18% EPS beat sent shares up 7% after hours. While FY 2026 guidance appears lower, this reflects normalization from Disney catch-up payments rather than business deterioration. The company's diversification into OTT and semiconductor markets continues to gain traction, with the Microsoft deal and RapidCool evaluations providing near-term catalysts.

Adeia reports earnings on February 23, 2026. View the full company profile.